How Much Does GAP Insurance Cost?

Free Car Insurance Comparison

Compare Quotes From Top Companies and Save

Daniel Walker

Licensed Insurance Agent

Dan Walker graduated with a BS in Administrative Management in 2005 and has been working in his family’s insurance agency, FCI Agency, for 15 years (BBB A+). He is licensed as an agent to write property and casualty insurance, including home, life, auto, umbrella, and dwelling fire insurance. He’s also been featured on sites like Reviews.com and Safeco. He reviews content, ensuring tha...

Licensed Insurance Agent

UPDATED: May 26, 2021

It’s all about you. We want to help you make the right coverage choices.

Advertiser Disclosure: We strive to help you make confident auto insurance decisions. Comparison shopping should be easy. We are not affiliated with any one auto insurance provider and cannot guarantee quotes from any single provider. Our partnerships don’t influence our content. Our opinions are our own. To compare quotes from many different companies please enter your ZIP code on this page to use the free quote tool. The more quotes you compare, the more chances to save.

Editorial Guidelines: We are a free online resource for anyone interested in learning more about auto insurance. Our goal is to be an objective, third-party resource for everything auto insurance-related. We update our site regularly, and all content is reviewed by auto insurance experts.

UPDATED: May 26, 2021

It’s all about you. We want to help you make the right coverage choices.

Advertiser Disclosure: We strive to help you make confident auto insurance decisions. Comparison shopping should be easy. We are not affiliated with any one auto insurance provider and cannot guarantee quotes from any single provider. Our partnerships don’t influence our content. Our opinions are our own. To compare quotes from many different companies please enter your ZIP code on this page to use the free quote tool. The more quotes you compare, the more chances to save.

On This Page

| Gap Insurance Basics | Details |

|---|---|

| Gap Insurance Variations | Return to Invoice Coverage New Car Replacement Coverage Loan and Lease Payoff Coverage |

| Where to Buy Gap Coverage | Primary Car Insurer Dealership |

| Cheapest At | Primary Car Insurer |

| Best For | New Cars with a Loan or Lease |

If you are interested in buying gap insurance but aren’t sure where to start, this guide is for you. It’s important to be aware of what gap insurance is and if it’s right for you before you start shopping. This way, you aren’t buying coverage that you don’t need, as car insurance is expensive enough.

If you’re wondering if gap insurance is worth it, this guide will help you reach a decision. Then, we will dive into which car insurance companies offer gap insurance and how to manage your policy once you have it.

Why is this so important?

Being aware of the small details of your policy and what each company offers will make sure you aren’t surprised by hidden conditions after an accident. The last thing you want is to purchase gap coverage and then have it fail you after your car is totaled.

So stick with us as we go through everything you need to know about buying and managing a gap policy from an insurer. If you would like to compare rates between insurers, you can enter your ZIP code in our free tool above.

Table of Contents

Car Insurance Companies with Gap Insurance Coverage

Now that you know everything about gap insurance and what it covers, it is time to dive into which companies offer gap insurance. Not all insurers offer gap coverage, so it’s important to check beforehand if you are switching to a new insurer and want gap insurance.

We will also go over the pros and cons of gap coverage to help you determine if you should gap coverage since it is only useful for certain drivers. And if you wondering if you should get gap insurance from an insurer or a dealership, don’t fear. We will address places to get gap insurance, so you can pick the provider that is best for you.

Ready to get started? Let’s jump into information about companies and gap coverage.

How much is GAP insurance

Gap insurance varies in cost, but if you are purchasing it from your primary insurer, it shouldn’t be more than an extra $100 a year (it will be much more expensive from a dealership). However, since you will need to also have comprehensive and collision coverage, you will have to pay more to add these coverages if you don’t have them already.

This means that your rate will look something like Quadrant’s data on the countrywide averages below.

| Coverage | Countrywide Average Premium |

|---|---|

| Liability | $516.39 |

| Collision | $299.73 |

| Comprehensive | $138.87 |

| Total Cost | $954.99 |

This is just the basic rate for people without driving offenses, poor credit scores, and basic coverages. Once you add on the cost of gap coverage and other add-on coverage, it will cost more. Still, this is a good guideline to go off of.

Of course, rates also vary by state. Take a look at the average cost of insurance by state below to determine how much your final cost should be.

| STATE | 2011 | 2012 | 2013 | 2014 | 2015 | Average |

|---|---|---|---|---|---|---|

| Alabama | $784.38 | $788.07 | $811.75 | $837.09 | $868.48 | $817.95 |

| Alaska | $1,053.48 | $1,053.54 | $1,058.15 | $1,050.09 | $1,027.75 | $1,048.60 |

| Arizona | $899.33 | $899.91 | $926.52 | $961.88 | $972.85 | $932.10 |

| Arkansas | $829.13 | $843.07 | $868.13 | $900.18 | $906.34 | $869.37 |

| California | $881.07 | $891.68 | $922.69 | $951.75 | $986.75 | $926.79 |

| Colorado | $835.50 | $849.74 | $887.57 | $939.52 | $981.64 | $898.79 |

| Connecticut | $1,068.18 | $1,082.28 | $1,109.03 | $1,132.78 | $1,151.07 | $1,108.67 |

| Delaware | $1,134.60 | $1,153.59 | $1,187.18 | $1,215.69 | $1,240.57 | $1,186.33 |

| District of Columbia | $1,276.99 | $1,289.49 | $1,316.48 | $1,324.39 | $1,330.73 | $1,307.62 |

| Florida | $1,160.13 | $1,196.57 | $1,209.70 | $1,208.77 | $1,257.13 | $1,206.46 |

| Georgia | $912.49 | $922.05 | $949.33 | $991.25 | $1,048.40 | $964.70 |

| Hawaii | $861.95 | $844.12 | $844.16 | $858.16 | $873.28 | $856.33 |

| Idaho | $641.96 | $639.19 | $650.57 | $673.13 | $679.89 | $656.95 |

| Illinois | $803.04 | $806.21 | $819.27 | $854.10 | $884.56 | $833.44 |

| Indiana | $710.36 | $724.44 | $704.50 | $728.93 | $755.03 | $724.65 |

| Iowa | $648.99 | $656.84 | $668.09 | $683.67 | $702.46 | $672.01 |

| Kansas | $780.43 | $785.72 | $815.82 | $850.79 | $862.93 | $819.14 |

| Kentucky | $872.48 | $888.46 | $904.99 | $917.49 | $938.51 | $904.39 |

| Louisiana | $1,281.55 | $1,275.10 | $1,307.72 | $1,364.17 | $1,405.36 | $1,326.78 |

| Maine | $662.28 | $667.66 | $674.94 | $689.12 | $703.82 | $679.56 |

| Maryland | $1,048.86 | $1,056.82 | $1,071.35 | $1,096.37 | $1,116.45 | $1,077.97 |

| Massachusetts | $1,011.14 | $1,048.06 | $1,080.48 | $1,107.76 | $1,129.29 | $1,075.35 |

| Michigan | $1,110.64 | $1,171.94 | $1,264.20 | $1,350.58 | $1,364.00 | $1,252.27 |

| Minnesota | $777.17 | $800.24 | $823.70 | $856.62 | $875.49 | $826.64 |

| Mississippi | $895.69 | $902.95 | $925.13 | $957.59 | $994.05 | $935.08 |

| Missouri | $790.27 | $799.14 | $819.79 | $845.39 | $872.43 | $825.40 |

| Montana | $816.21 | $821.68 | $842.74 | $868.55 | $863.52 | $842.54 |

| Nebraska | $732.21 | $751.18 | $773.64 | $805.99 | $831.02 | $778.81 |

| Nevada | $1,029.87 | $1,024.09 | $1,047.74 | $1,083.42 | $1,103.05 | $1,057.63 |

| New Hampshire | $746.57 | $755.76 | $773.30 | $795.50 | $818.75 | $777.98 |

| New Jersey | $1,303.52 | $1,334.59 | $1,369.70 | $1,379.20 | $1,382.79 | $1,353.96 |

| New Mexico | $869.85 | $866.19 | $888.83 | $920.42 | $937.59 | $896.58 |

| New York | $1,236.77 | $1,273.70 | $1,301.49 | $1,327.82 | $1,360.66 | $1,300.09 |

| North Carolina | $708.10 | $720.47 | $739.91 | $768.28 | $789.09 | $745.17 |

| North Dakota | $688.74 | $714.75 | $743.27 | $768.09 | $773.30 | $737.63 |

| Ohio | $697.61 | $714.05 | $738.68 | $766.66 | $788.56 | $741.11 |

| Oklahoma | $881.50 | $902.90 | $931.41 | $985.58 | $1,005.32 | $941.34 |

| Oregon | $804.59 | $818.07 | $856.26 | $894.10 | $904.83 | $855.57 |

| Pennsylvania | $904.47 | $915.83 | $930.48 | $950.42 | $970.51 | $934.34 |

| Rhode Island | $1,148.97 | $1,176.05 | $1,210.55 | $1,257.40 | $1,303.50 | $1,219.29 |

| South Carolina | $857.70 | $880.82 | $904.22 | $936.69 | $973.10 | $910.51 |

| South Dakota | $669.20 | $690.95 | $717.30 | $744.28 | $766.91 | $717.73 |

| Tennessee | $767.82 | $794.53 | $829.38 | $855.56 | $871.43 | $823.74 |

| Texas | $959.87 | $974.68 | $1,017.81 | $1,066.20 | $1,109.66 | $1,025.64 |

| Utah | $809.35 | $805.32 | $820.92 | $852.66 | $872.93 | $832.24 |

| Vermont | $716.14 | $726.57 | $734.82 | $746.79 | $764.02 | $737.67 |

| Virginia | $768.95 | $781.38 | $809.40 | $836.14 | $842.67 | $807.71 |

| Washington | $889.82 | $891.04 | $914.04 | $952.10 | $968.80 | $923.16 |

| West Virginia | $992.57 | $1,005.68 | $1,021.37 | $1,032.45 | $1,025.78 | $1,015.57 |

| Wisconsin | $669.99 | $666.79 | $689.77 | $716.83 | $737.18 | $696.11 |

| Wyoming | $791.14 | $796.14 | $804.52 | $844.33 | $847.44 | $816.71 |

| Countrywide | $908.43 | $924.45 | $950.92 | $981.77 | $1,009.38 | $954.99 |

Once you find your state’s average (assuming you have liability, collision, and comprehensive coverages), you can expect to pay this at minimum. Once you add in the cost of any add-ons you have, including gap coverage, it will be at least a few hundred more than the basic average.

Which car insurance companies have gap coverage?

We went through the most popular car insurance companies to find out which ones offer gap insurance (or similar types of coverage). Take a look at the table below to see which companies offer protection for your new car.

| Company | Gap Coverage | New Car Replacement | Loan or Lease Payoff |

|---|---|---|---|

| Allstate | Covers vehicles valued/financed up to $100,000. | Car must be two model years old or less. | No |

| American Family | Yes (called loan/lease gap at American Family but does cover total loss). | No | No |

| Esurance | No | No | Up to 25 percent of car's actual cash value. |

| Farmers | Yes | Car must be two model years old or less and less than 24,000 miles. | No |

| Liberty Mutual | Yes | Car must be under one model year old and less than 15,000 miles. | No |

| Nationwide | Yes | No | No |

| Progressive | Yes (called loan/lease payoff at Progressive but does cover total loss). | No | No |

| Travelers | Yes | Car must be five years old or less. | No |

Insurers have different regulations when it comes to new car replacement, such as how old the car is allowed to be and how many miles can be on it. So make sure to ask your insurer how long new car replacement or gap coverage will be valid on your vehicle.

You may have noticed that a few major insurers are missing on the above list, such as Geico, State Farm, and USAA. Currently, these companies do not have gap coverage, although they may add it in the future.

Compare quotes from the top auto insurance companies and save!

Should I get gap car insurance coverage?

Only you can answer that question, but we will help you get there by going through some of the pros and cons of gap coverages before diving into situations when you should/shouldn’t have gap coverage.

| Pros | Cons |

|---|---|

| Will make sure you don't suffer a loss. | Only covers newer vehicles. |

| Only covers the gap in price for totaled cars. | Won't cover repairs or injury costs. |

| Isn't that expensive to add on. | Will still have to buy comprehensive and collision coverage in addition to gap coverage. |

So what are some of the situations where you should get gap coverage? According to III, you should get gap coverage if:

- You “made less than a 20 percent down payment” on your car.

- You “financed for 60 months or longer.”

- You “leased the vehicle (carrying gap insurance is generally required for a lease).”

- You “purchased a vehicle that depreciates faster than the average.”

- You “rolled over negative equity from an old car loan into the new loan.”

In all these situations, you would suffer a heavy loss if your car was totaled and you didn’t have gap insurance. You may also be required to purchase gap coverage when you sign a lease agreement, although gap coverage is usually optional. The video below shows why gap insurance is so important when drivers have auto loans.

However, there are some situations where you don’t need gap coverage. According to NOLO, “you don’t need to consider gap protection if, during your loan term or lease, you will not owe more than your car is worth.”

In addition, if your car is more than a few years old and your loan/lease is paid off, you probably don’t need gap coverage. If you are on the fence, try to calculate how much you would be stuck paying on your vehicle by looking at what is left on your loan/lease and the actual cash value of your car.

Should I buy gap coverage from my insurer or a dealership?

This is a question many people ask when buying a new car, as not all insurers offer gap insurance. However, it can be more expensive to buy gap insurance from a dealership.

This is because a dealership won’t have the discounts that are available at a provider and the insurance is being sold as a standalone product. Whereas if you add gap insurance onto your plan at your insurer, your rate won’t go up too much. View the video below to learn more about where to buy gap insurance.

Gap insurance from a dealership is also not regulated by the state, which means dealerships can charge more than insurers (who have to run rates by state officials).

Another factor to consider is that even if you have two separate policies — primary insurance at your regular provider and gap insurance from a dealership — this doesn’t mean you are doubly covered. So if your primary insurer denies your claim, gap coverage from the dealership will also be denied.

This is why it’s important to have all your basic coverages on your car before buying gap coverage. Otherwise, your claim will be denied and your gap insurance won’t go through.

The Basics of Gap Car Insurance

Not sure if gap car insurance is right for you? Or maybe you’ve heard of gap insurance but aren’t sure what exactly it is? If you have questions about gap insurance, this section is for you.

We will cover everything you need to know about the differences between gap coverages and what will and won’t be covered by your policy. Let’s get started.

What is gap car insurance?

GAP is short for Guaranteed Asset Protection. This insurance an add-on policy for new cars that have been loaned or leased. It protects your investment in case your car is totaled, as your car won’t be worth as much as when you first bought it.

According to the Insurance Information Institute (III), “When you buy or lease a new car or truck, the vehicle starts to depreciate in value the moment it leaves the car lot. In fact, most cars lose 20 percent of their value within a year.”

So if you total your car, your insurance will only pay you what your car is currently worth. This is where a basic gap insurance steps in and pays for the gap between the actual (depreciated) value of your totaled car and what you still owe on your loan or lease.

Why is this worth it?

If you don’t have gap insurance, you may be stuck making loan or lease payments on a car currently in the junkyard. So gap coverage makes sure that your assets are protected and that you won’t face losses after a car accident. Watch the video below for a quick overview of the basics of gap coverage.

https://youtu.be/4ZQmb_L1Hxk

Now that you have the basics of gap coverage down, let’s dive into the different types of gap that are offered at most insurers.

What are the different types of gap car insurance?

There are actually a few different variations of gap insurance. While only one is considered true gap insurance — return to invoice gap — there are other variations of gap coverage that some companies will use interchangeably.

While all of them serve the same basic function — making sure you don’t suffer losses — they are different in how they approach the issue.

As a result, some types of gap coverage will cover you more completely after an accident, while others will only cover a portion of your costs.

To make sure you get the type that is right for you, keep reading to learn about return to invoice gap, vehicle replacement gap, and loan/lease payoff gap.

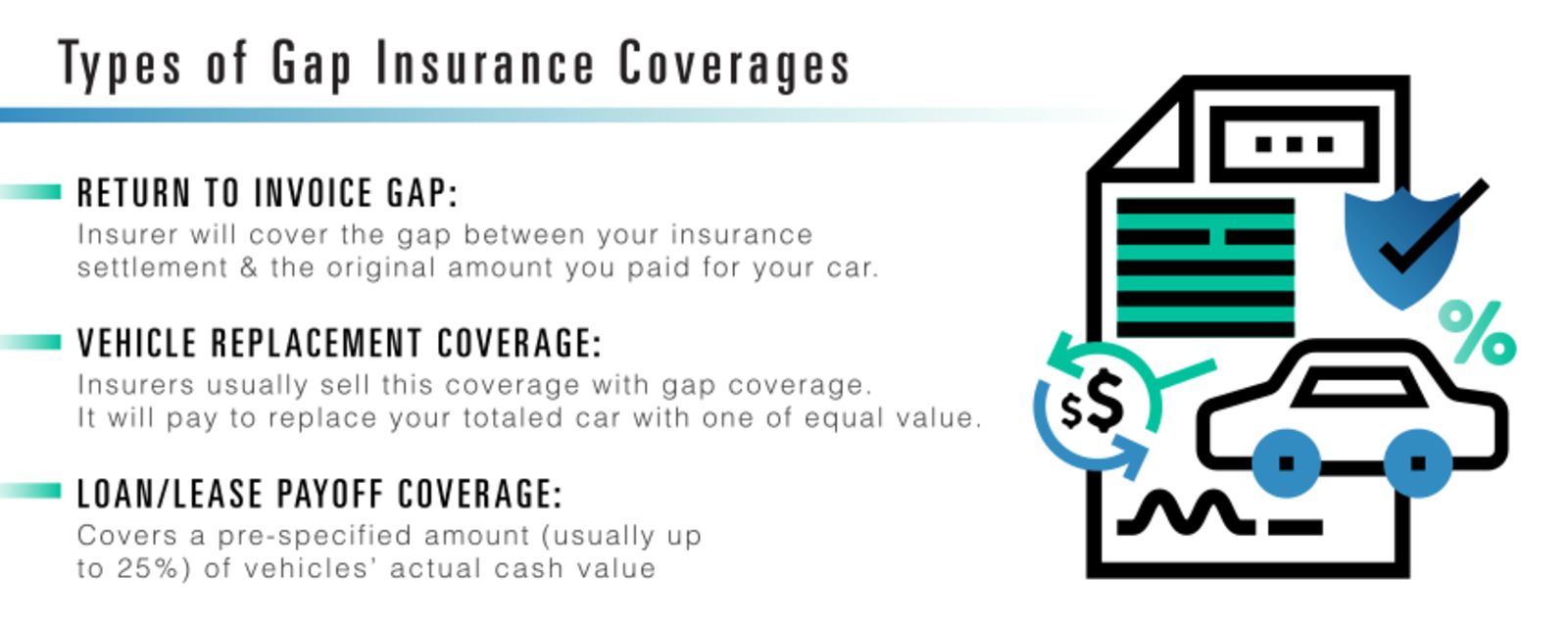

Return to Invoice Gap

This is the type of coverage that most people think of when considering gap insurance. Basically, return to invoice gap pays the difference between your settlement and what you originally paid for your new car.

So if you total your brand new car only a month after buying it for $30,000, but your settlement only gave you $25,000, gap will cover the $5,000 difference so that you aren’t stuck with a loss on your asset.

Even if you don’t think you are likely to get into a crash, this gap insurance is still worth it. The last thing you want is to be stuck with a financial loss when trying to find a new car to replace your totaled car.

Vehicle Replacement Gap

This type of coverage works slightly differently than your basic gap coverage. Typically called new vehicle replacement at most insurers, this coverage will help out if your new vehicle is totaled and considered a total loss. The video below shows a typical example of a new car replacement policy at an insurer.

https://youtu.be/mZwgIPmeglw

New vehicle replacement will pay for a new car that is the same make and model as your destroyed one, as long as your totaled car is unfixable and declared a total loss. However, you will generally need to have collision and comprehensive coverage in order to get new vehicle replacement insurance.

- Collision coverage will cover the costs of a collision with another vehicle or object (such as a mailbox or fence).

- Comprehensive coverage will cover the costs of damages from natural disasters, animal collisions, vandalism, and theft.

Because you usually need comprehensive coverage with new vehicle replacement coverage, this means that a stolen car would also count under this insurance, not just totaled cars.

Loan and Lease Payoff Gap

Loan and lease payoff is commonly confused with basic gap insurance, but it is markedly different. While this coverage does help with some of your expenses, it will not completely cover your losses.

Generally, loan and lease payoff will cover a pre-specified percentage of the actual value of your vehicle (what you paid for it before driving it off the lot). This pre-determined rate is fairly low, usually no more than 25 percent. So if you paid $40,000 for your new vehicle, loan and lease payoff will only cover $10,000 of your vehicle’s actual value.

This means that unlike true gap insurance, loan and lease payoff will probably leave you with some bills you’ll have to pay yourself. So don’t confuse the two, as getting the wrong coverage could cost you later.

What does gap car insurance cover?

While we covered the basics of what these coverages do, you are probably wondering what exactly true gap coverage will protect. Because new car replacement and loan/lease coverages are straightforward, in this section we will be solely talking about basic gap coverage, which offers the most complete coverage.

So if you want to know if what types of cars and wrecks gap insurance will cover, keep reading. We will cover all types of situations that you may find yourself needing gap coverage for.

What types of cars does gap car insurance cover?

Every insurer is different, but your car must be new. You can’t get gap insurance on a decade-old car, but you should be able to get gap insurance on a two-year-old car.

This is because the depreciated value of an old car would be a significant loss of money to an insurer, not to mention that the loan or lease is probably close to being paid off.

Gap insurance also won’t completely cover modified cars, as you have changed the value of the car by adding new engines, a custom paint job, or any other major modification. In some cases, insurers may not offer gap insurance at all to modified cars. It really just depends on the insurer.

If your gap insurance doesn’t completely cover your modified car, your best bet is to purchased modified insurance in addition to gap insurance. Modified car insurance will cover the cost of modified replacement parts if yours are damaged or stolen. However, it can be a little harder to find modified car insurance, so you may not be able to combine it with gap insurance easily.

Still, it is worth the effort to avoid having to pay out of pocket.

Another question people frequently ask is if gap insurance will cover rental cars. The answer to this is no. Gap insurance will not apply to rental cars if you total a rental car, nor will it cover the cost of a rental vehicle after a gap insurance claim.

In fact, at most insurers, you will need to have rental coverage in order to receive a rental car after a claim. Otherwise, you will have to pay out of pocket while your car is repaired or you shop for a new car.

What types of wrecks and situations does gap insurance cover?

You may be wondering what exactly gap insurance will cover after an accident. Let’s go through some of the more commonly asked questions about gap insurance.

Does gap insurance cover a car totaled in an accident? Yes, this is what gap insurance was created for. Gap insurance is usually sold along with collision or comprehensive coverage, so it will cover the difference between the actual value of a totaled or stolen car and what is left on your loan or lease. If you have new car replacement insurance, you will be covered to buy a new vehicle of the same make and model as your old one.

Does gap insurance cover car repairs? Gap insurance will not pay for car repairs. Remember, it is only intended to cover the difference between what you paid for your car and its depreciated value after it is totaled. Your other coverages, such as collision and comprehensive, will cover the repairs to your vehicle.

Does gap insurance cover me if my car is not totaled? Your car must be a total loss for gap coverage to kick in. This means that gap insurance will also cover car thefts (as long as you have comprehensive coverage). If your car isn’t a total loss after an accident, then gap insurance won’t cover anything and your other coverages will cover repairs. Watch the video below to learn more about the basics of gap insurance and totaled cars.

Will gap insurance replace my vehicle? Standard gap coverage will only cover the gap between what you paid and the depreciated value of the car. While you can put this money towards buying a new vehicle, the only type of insurance that directly gives you a settlement for a new car is new car replacement insurance.

No matter which insurer you pick, the basics of how gap insurance work are the same at every insurer. Just make sure you’re aware of what type of coverage you are purchasing, as new car replacement won’t be the same as true gap coverage.

Does gap insurance cover damages if I’m at fault?

This is a tricky question, as an insurer will cover you even if you were at fault. But the repercussions partially depend on whether you live in an at-fault or no-fault state.

A no-fault state means that each driver’s own insurer will cover their cost of repairs, regardless of who caused the accident. According to the III, the following states are no-fault or have some type of no-fault coverage: Florida, Michigan, New Jersey, New York, Pennsylvania, Hawaii, Kansas, Kentucky, Massachusetts, Minnesota, North Dakota, and Utah.

In an at-fault state, whoever caused the accident is responsible for the other driver’s medical and property damage bills. So while your insurer will probably cover your gap insurance claim in both types of state, if you were at fault, this will raise your insurance rates. If you weren’t at fault in an at-fault state, the other driver is responsible for your costs.

Still, it’s smart to have gap insurance and uninsured/underinsured coverage. A driver may have poor insurance or no insurance, forcing you to pay for your own repairs. Uninsured and underinsured will cover you in these instances, and gap insurance will make sure that you aren’t suffering a loss.

What isn’t typically covered by gap insurance?

Gap insurance is fairly straightforward, but there are still some things to clear up about gap insurance doesn’t cover. Let’s go through some of the questions consumers ask about gap insurance coverage and why these situations aren’t covered under gap insurance.

Does gap insurance cover bodily injury or death? Gap insurance will not cover the costs of injuries or death after an accident. Gap insurance is solely for the gap in costs on your vehicle.

Does gap insurance cover my down payment? Gap insurance doesn’t cover downpayment, which is why it’s good to get gap insurance if you made a small downpayment or no downpayment. If you made a large downpayment, then regular insurance should be enough to cover you.

Does gap insurance cover trade-in value? Some people want to trade-in their vehicles to get the newest, latest model. Gap insurance doesn’t apply to these trade-ins, as the car was not totaled or stolen. Even if your car is a total loss, gap insurance won’t give you more money to upgrade. And if you have new car replacement, you will only get a settlement for a car of the same model and value.

Does gap insurance cover deductibles? Gap insurance doesn’t cover deductibles, as a deductible is the amount you agree to pay in an accident. So if you have a $500 deductible, you will have to pay $500 towards repairs or replacement before your insurer steps in to cover the rest.

Gap insurance just covers the basic difference in value on your vehicle. If you want more coverage, such as injury coverage, you will have to invest in other add-ons.

Managing Your Gap Car Insurance Policy

Now that we’ve covered what gap insurance is and whether you should get gap insurance, it is time to dive into all the tips and tricks of managing your gap insurance policy.

When we say this, we don’t mean knowing your way around your insurers’ apps and discounts. Rather, we want to talk about payments, canceling gap insurance (and when you should cancel it), and reasons why your claim might be denied. We will also discuss when you should and can buy gap insurance, whether right on the lot or years after buying your new car.

So keep reading for a detailed look at how to get the best use out of your gap insurance policy.

Will making a late payment void my gap car insurance policy?

This is a common concern most people have after forgetting to make a payment. Fortunately, most car insurance companies have a grace period (usually 10 to 15 days, though it may be much shorter). So as long as you make your payment within your grace period, your insurer won’t cancel your car insurance.

If your car insurance is canceled, you will face what is called a lapse in insurance. These lapses are seen by providers and can make it harder to find an insurer. At the very least, you will face increases in rates.

Another concern people have is that if they miss a payment on their car insurance loan or lease, their gap car insurance will be void. However, missing payments on your car won’t cancel your gap car insurance. If your car is totaled, though, gap insurance won’t cover the cost of your late payments.

So make sure to stay on top of both your car insurance payments and your car payments. Otherwise, it could cost you a great deal of money later.

What if I want to cancel my gap car insurance policy?

If paying for gap insurance is no longer worth the return value, it may be time to cancel your policy. Common reasons for canceling are:

- Your overall policy becomes more expensive. If this is the case, try ways to save on car insurance if you still want gap coverage, such as taking advantage of discounts or shopping for a new insurer.

- Your loan or lease is paid off. Now is the time to cancel, as you no longer have to worry about owing anything if your car is totaled.

When you do cancel your policy, you should receive a refund for any unused coverage. So if you pay for a year of gap coverage but cancel your gap coverage six months in, you should be refunded the remaining amount.

Still have questions about canceling your policy? Keep reading for advice on when to drop your policy and what happens when you cancel.

Should I cancel my gap insurance if I refinance my auto loan?

Wells Fargo Bank describes auto refinancing as “An auto refinance loan is a secured loan used to pay the existing balance on a current car loan. The car is used as collateral for the new refinanced loan. The refinanced car loan has a fixed interest rate and fixed monthly payments for a set period of time.”

So refinancing your loan is a way to change how much you pay each month and what your interest rate is, which may help your finances in the long run. Still not clear on how refinancing works? The video below further explains the basics of refinancing.

However, your current gap insurance policy will usually end when you refinance your vehicle. You will have to purchase a new gap policy to go with your new, refinanced loan.

Why?

Because your insurer will need to evaluate the difference between the actual value of your car and what you would have left on your loan. So if you change your loan or lease, you need a new gap policy.

Can you cancel gap insurance from a dealership?

Yes, you can always cancel your gap insurance unless it was a stipulation on your lease. If you paid off your lease, though, your dealership must let you cancel your gap insurance.

Just make sure that you truly don’t need gap insurance before canceling it. The last thing you want is to total your car and lose money because you didn’t have gap insurance.

Can you cancel your gap insurance from a car loan?

Yes, you can cancel your gap insurance from a car loan. However, you want to make sure that you are close to paying off your loan before you cancel. In the off chance that you total your vehicle before your loan is mostly paid off, you will be stuck with a large portion of the losses.

So make sure to double-check your finances and your loan before canceling.

What happens if you cancel your gap insurance?

You will no longer be protected if your car is totaled and you still owe money on your loan or lease. This is why it’s important to consider if it’s the right time to cancel.

You will also want to make sure that your insurer cancels your gap insurance properly. To make sure, check your bill next month and make sure that the cost for gap insurance has been taken off. If it hasn’t, give your insurer a call right away.

This is because mistakes happen, and the last thing anyone needs is to be charged for coverage they thought they dropped.

Can my insurer deny my gap car insurance claim?

An insurer can always deny your claim, especially if an insurer believes a claim is fraudulent. Other common reasons for claim denial, according to Staver Accident Injury Lawyers, are:

- There is an unclear case of disputed liability. “The insurance company may say that their policyholder didn’t cause the accident, or that the accident didn’t cause the injuries or damages you’re claiming.”

- Your policy doesn’t cover the accident. “Insurance policies usually include a laundry list of items that aren’t covered. A lot of people have heard that an insurance policy won’t cover an ‘act of god,’ for example. Another example is intentional actions, which often are not covered by insurance policies. The company may use one of those items on the list, known as exclusions, to say that your accident isn’t covered by their policy.”

- Your policy lapsed. “If the premiums hadn’t been paid at the time of the accident, the policy may have lapsed and the insurance company would say that no coverage existed at the time of the accident.”

- You failed to notify your insurer.” Policyholders have an obligation to notify insurance companies of accidents in a reasonable amount of time after the accident happened. If that didn’t happen, the insurance company may claim it didn’t have an opportunity to investigate the accident and may deny the claim.”

These are the most basic, and usually valid, reasons why your insurer might deny your claim. If you want more information on how to avoid a denied claim, watch the video below.

If you feel your claim was unjustly denied, such as your insurer not fulfilling their contract obligations, the next step is to contact a lawyer to see if you have a case.

Remember, your gap insurance won’t be paid, even by a dealership, if your primary insurer denies your claim. So if you have a strong case, it may be worth it to pursue action in order to get the money you are owed.

When should I buy gap insurance?

You can buy gap insurance at any time, but it is best to buy gap insurance shortly after purchasing a car that has a loan or lease. This is because when you near the end of your loan or lease, it is about time to cancel your gap insurance. So if you are looking to buy gap when you only have a few months left on your loan or lease, it’s probably not worth it.

Remember, your car stops dropping in value the moment you drive it off the lot, so the sooner you get gap insurance the better. It’s probably not worth getting gap insurance if it’s been a few years since you bought your car, but it’s worth getting gap insurance if you just bought your car a few months or even a year ago.

If you are having trouble doing the math to find out the value of your car and your loan/lease prices, it always helps to talk to a financial advisor who can figure out the cost of gap insurance for you. However, gap insurance really does only add on a little extra to your basic insurance policy, making it a wise investment for most drivers and their cars.

Gap Car Insurance FAQs

We’ve covered a lot of roadway in this guide about gap insurance coverage. However, there is always more to ask about this coverage. If you still have a few lingering questions, stick with us for this last section.

To give you the best information possible, even at the end of our guide, we went through and answered the most frequently asked questions about gap car insurance. Take a look below.

What happens if you have gap car insurance but end up paying off your car loan early?

Got ahead on your loan payments and no longer need gap insurance? You can certainly cancel your gap car insurance if you paid off your car loan early. Your insurer should refund you for the unused gap insurance if you prepaid for coverage. Just make sure to doublecheck that the cancellation went through.

Can I transfer gap insurance to another car?

No, you can not transfer your gap insurance policy to another car. Every car would require a new gap insurance policy, as it is a special add-on coverage. So you can’t take your gap insurance off your four-year-old car and put it on your one-year-old car.

However, you can certainly cancel your current policy on one car and buy a new policy for your other car. This way you won’t be paying gap insurance policies for two cars. Just make sure that if you cancel one policy you aren’t putting yourself at risk of financial loss.

Is gap car insurance required?

Not unless it is a condition on your lease. Sometimes dealerships will make purchasing gap insurance a condition of signing a lease. This is why it’s always important to check the fine print. Since gap coverage from dealerships costs more, see if you can purchase gap from your primary insurer before buying from a dealership.

Remember, a dealership will still reject your claim if your primary insurer rejected your claim, so having insurance in two places won’t ensure you get paid after an accident.

Other than that, gap car insurance is completely optional. In addition, because it is usually an add-on, it doesn’t cost an arm and a leg to add to your main policy.

Can I buy gap car insurance if I don’t have basic insurance?

No. You need to follow your state’s regulations on mandatory liability insurance before you can buy gap car insurance. Most insurers also require you to have comprehensive and collision coverage to have gap insurance, otherwise, your gap claim may be denied.

Bottom line? Gap car insurance is an add-on product, not a stand-alone coverage. You need to have basic coverage on your vehicle to have gap insurance, though we always recommend having as much coverage as possible to better protect in an accident.

Can I buy gap car insurance for a used vehicle?

Yes, as long as you owe a loan or lease on a car you can usually buy gap car insurance from most providers. However, you won’t be able to get new car replacement insurance, as a used vehicle is usually past the cutoff date.

As a reminder, usually, this cutoff date requires that a vehicle must be two model years old or less. The longest cutoff date listed is a five-year-old vehicle, but this cutoff date is rare.

Can I use my gap insurance as proof of insurance?

Since states require proof of insurance, you may be wondering if you can show your gap insurance coverage as proof. However, this is not sufficient proof. You need proof that you have the basic car insurance required by your state, whereas a gap insurance statement is merely proof of an optional coverage.

So make sure you have your paperwork in order, as you will need proof of insurance at traffic stops, when registering a car, or when you are in an accident. Insurers will generally issue a proof of insurance card within one to two weeks of your policy purchase.

Do I need gap insurance if someone other than a bank or financer has my loan?

If you got your loan through a private person, insurers usually won’t sell you gap insurance. This may seem unfair, but insurers need detailed proof of the loan through official channels to make sure the loans aren’t fraudulent. For example, someone may try to claim they have a $50,000 loan on a $20,000 car.

You’ve stuck with us the whole way, and we hope we answered all your questions about the basics of gap insurance and where you can buy it from. Our hope is that you feel comfortable with the ins and outs of gap insurance and are ready to make your purchase (or cancel your policy).

To start comparison shopping for car insurance rates today, you can enter your ZIP code in our free online tool below.

References:

- https://www.iii.org/article/what-gap-insurance

- https://www.iii.org/article/background-on-no-fault-auto-insurance

- https://www.quadinfo.com/

- https://www.wellsfargo.com/auto-loans/auto-refinancing/

- https://www.chicagolawyer.com/auto-accident-personal-injury-resources/what-happens-if-your-insurance-claim-is-denied/

- https://www.chicagolawyer.com/car-accident-lawyer/insurance-issues/disputed-liability/

- https://www.chicagolawyer.com/car-accident-lawyer/insurance-issues/exclusions/

- https://www.chicagolawyer.com/car-accident-lawyer/insurance-issues/

- https://www.chicagolawyer.com/car-accident-lawyer/insurance-issues/failure-to-notify/

FREE Auto Insurance Comparison

Compare quotes from the top auto insurance companies and save!

Daniel Walker

Licensed Insurance Agent

Dan Walker graduated with a BS in Administrative Management in 2005 and has been working in his family’s insurance agency, FCI Agency, for 15 years (BBB A+). He is licensed as an agent to write property and casualty insurance, including home, life, auto, umbrella, and dwelling fire insurance. He’s also been featured on sites like Reviews.com and Safeco. He reviews content, ensuring tha...

Licensed Insurance Agent

Editorial Guidelines: We are a free online resource for anyone interested in learning more about auto insurance. Our goal is to be an objective, third-party resource for everything auto insurance-related. We update our site regularly, and all content is reviewed by auto insurance experts.